The Future of Auto Insurance

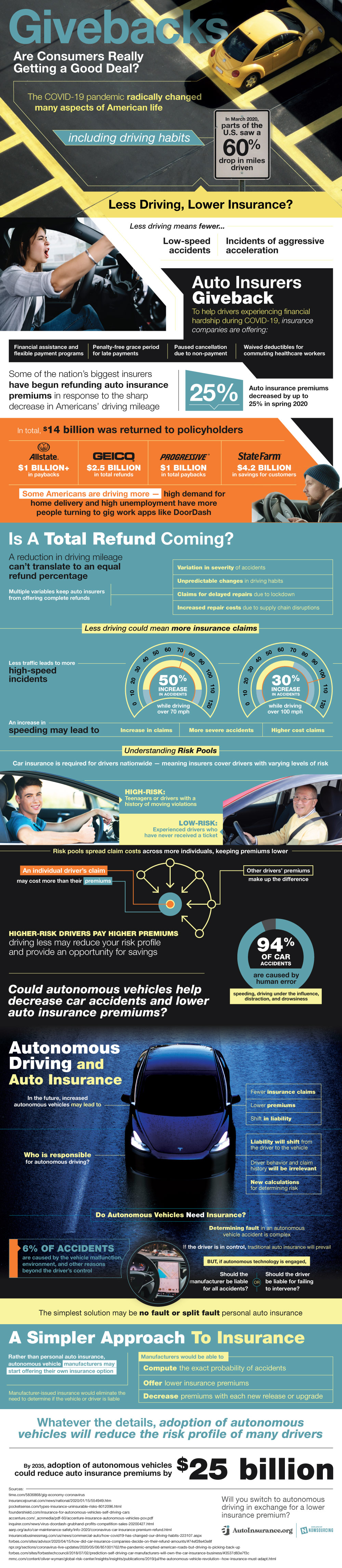

Many things changed during 2020 due to the COVID-19 pandemic. One major change came to how Americans are driving. In March, there was a 60 percent drop in mileage. Less driving means less low-speed accidents. In addition to less driving and accidents, many Americans are now facing financial struggles due to the pandemic. Many auto insurers are offering ways to help their policyholders—they have offered financial assistance and flexible payment programs, penalty-free grace period for late payments, paused cancellation due to non-payment, and waived deductibles for commuting healthcare workers. Some of the bigger companies like State Farm and GEICO have even offered to refund premiums in response to the drop in mileage. This totaled $14 billion in givebacks.

It is also important to note that some Americans are driving now more than ever. With the financial struggles brought on by the pandemic, many people have turned to gig work apps like DoorDash to make money. This has increased mileage for many drivers.

With these things in mind, would the refunds ever reach 100 percent back?

Unfortunately, it will most likely not happen. There are multiple variables that go into insurance and that keep insurers from offering full refunds. These include: variation in severity of accidents, increased repair costs due to supply chain disruptions, claims for delayed repairs due to lockdown, and unpredictable changes in driving habits.

In addition to these factors, there is also the fact that driving less could mean more insurance claims. With less cars on the road, there is less traffic. Less traffic means more speeding and a higher chance of high-speed accidents. There was a 50 percent increase in accidents while driving over 70 mph and 30 percent increase in accidents over 100 mph. An increase in speeding could lead to this as well as an increase in claims and higher cost claims.

Along with the pandemic, auto insurance could also change due to the introduction of autonomous vehicles. Considering 94 percent of accidents are caused by human error, autonomous vehicles could decrease accidents and lower risks involved in driving. However, when there is an accident, the big question is who is liable—the driver or the manufacturer?

It is a complex question, but one way to simplify it is to have the vehicle manufacturer provide the insurance instead of traditional auto insurance providers. They manufacturer would be able to calculate the exact likelihood of a crash and factor that into the price. This could drastically lower premiums.

Adopting autonomous vehicles could reduce premiums by $25 billion by 2035.